If you’re dabbling in investments and aspire to grow your portfolio, it’s important to understand your risk appetite and invest in line with your financial situation and individual risk tolerance.

While it’s true that every kind of investment come with risks, the level of risk varies depending on the asset class, so it’s up to you to ensure your investment portfolio matches your risk profile.

A financial adviser can help you determine your risk appetite and ensure you are confident in making investment decisions that not only align with your risk tolerance but also with your financial goals.

Tips on Building an Investment Portfolio that Suits Your Risk Tolerance

Tip #1: Know Your Risk Tolerance

Your risk tolerance level will determine how much investment risk you are willing to take to earn a higher return. The higher your risk tolerance is, the greater your potential to earn higher returns. However, bear in mind that the higher you set your risk appetite, you usually risk losing more money as well.

You can gauge your risk tolerance by answering the following questions:

- Are you comfortable with investing in stocks and other equity-oriented investments even if that means you might lose some money?

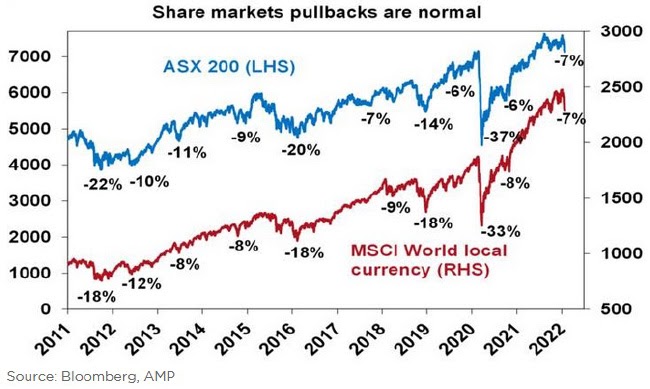

- Are you comfortable losing 30-50% of your money overnight in a falling market even if you have time to wait until the market recovers in the long term?

- Would you be more comfortable with investing in a fixed income product that has relatively lower returns than other products?

- What are your financial goals and investment goals? Do you have short term or long term investment goals?

Smart investors match their investments with their lifestyle and financial goals.

For example:

- If you are investing for a house you want to buy in the next 3 years, it may make sense to choose a low-risk investment that does not experience much market volatility. This would be a more conservative portfolio – meaning you can be more certain of your investment returns and enjoy financial security in the short term.

If you are investing for retirement and planning to retire 15+ years down the track, you may have a higher risk tolerance. You may be comfortable taking greater risk in more volatile markets if it means your money will grow more over the long term.

Tip #2: Take Time to Learn about Investment Options

Your investment options are endless.

Before investing in a particular asset class, you should be aware of how it works, how the returns are generated, what the risks are and what the tax implications are. Different asset classes hold different risks. The right asset classes for you to build a diversified portfolio will depend on your financial situation.

If you are new to investing, consider talking to a financial adviser about your investment strategy and how you can match your strategy with an evidence-based market activist as well as your high or low-risk tolerance.

Tip #3: Learn About Asset Classes and Asset Allocation

Asset allocation refers to how you divide your portfolio between different types of investments. For example, you can divide your portfolio between fixed income products, equity products, property and other types of investments.

A well-diversified portfolio will generally carry lower risk as your assets are protected by short term losses by your other assets and investments.

The performance of each type of investment is different so you need to allocate your portfolio in a way that will help you achieve your target returns. However, you might need to tweak your asset allocation regularly depending on how financial markets perform.

Managing Risks and Building a Balanced Investment Portfolio

Your investment portfolio will usually contain a mix of investments that are likely safer than others. For example, you can invest in mutual funds, bonds, stocks, ETFs and other investment vehicles that are relatively safe.

Regardless of how you decide to invest, make sure you account for your levels of risk tolerance, investing goals and time horizon. Diversify your portfolio to reduce risk and help balance your investment portfolio.

How Can A Financial Adviser Help You?

If you’re planning your investment strategy and matching it to your risk appetite, seek investment advice from a qualified financial planner.

It’s best to work with a reliable financial adviser in Hornsby who can help you secure your financial future.

Hyland Financial Planning aims to build a collaborative partnership with clients to help them build and protect their wealth through strategic financial planning and creation. Our goal is to help you reach success – no matter what success looks like to you.